Introduction

-

We should draw a clear distinction at the outset between two separate, albeit related, concepts.

-

As I set out in my last series of blogs, one method of ensuring that a nation’s carbon emissions reduce over time is by constructing a ‘cap and trade’ system in which significant emitters are provided with an ever reducing cap on the annual amount of CO2 equivalent they may produce. This amount is represented by an equivalent number of allowances (usually supplied to the emitter free of charge by the regulating authority). If, through its own efficiencies an emitter finds that it has spare unused allowances at the end of the accounting period, then it may trade them for value to another emitter whose emissions would otherwise exceed their own allowance and incur fines more expensive than the cost of buying the spare unused allowances. This is ‘carbon trading’.

-

At the stage prior to considering whether allowances need to be purchased to cover its reported annual emissions, an emitter may be able to nett off from its actual ‘gross’ emissions, permitted ‘carbon credits’ which it has purchased from elsewhere and to ‘offset’ those credits from its gross emissions total in order to arrive at a nett emissions total. It is then this nett total which is tested against the number of emissions allowances allocated to the emitter. This is ‘offsetting’. It will be recalled that, in principle, these carbon credits arise from the activities of others in other parts of the world and who have been paid by the emitter to either reduce their own emissions or to increase their own carbon capture in a way which they would not have done but for the emitter’s instruction.

-

This is a huge and complex area because not only must the interface between carbon trading and carbon offsetting be understood, there exist several layers and areas of carbon trading i.e. the UK’s involvement in the EU-ETS (under Kyoto); the coming into force of CORSIA in respect of the airline industry and that is before the effects of EU withdrawal are considered.

-

This blog only deals with the carbon trading system insofar as it is necessary to understand what I really want to talk about, namely offsetting. The other aspects will remain for other blogs. But even within the limited area of offsetting, I have to be even more selective in order to keep the length of any one blog manageable and so I will not, in this one, deal with CORSIA.

-

So, this blog considers solely the domestic (i.e. non-EU and non-UN/CORSIA) systems of permitting carbon offsetting which pertain up until our exit day 31.12.20

To begin at the beginning……

-

The wellspring statute is, of course, the Climate Change Act 2008. This is a wide-ranging piece of legislation, but for our purposes, it required the UK to commit to an overall ‘target’ goal of achieving net carbon neutrality by 2050 and to do so by reducing national carbon emissions in graduated 5 year periods via the setting of a CO2 equivalent annual limit known as the ‘carbon budget’. The reductions were calculated as a reducing percentage of the baseline of UK emissions in 1990. (ss 1, 4-5 of the 2008 Act). For the sake of completeness, the budget periods for which limits have been set so far have been:

|

Budget |

Period |

Limit (MtCO2e) |

% below 1990 baseline |

Enacting Legislation |

|

1st |

2008-2012 |

3,018 |

25 |

Carbon Budgets Order 2009 (SI 2009/1259) |

|

2nd |

2013-2017 |

2,782 |

31 |

Ditto |

|

3rd |

2018-2022 |

2,544 |

37 |

Ditto |

|

4th |

2023-2027 |

1,950 |

51 |

Carbon Budget Order 2011 (SI 2011/1603) |

|

5th |

2028-2032 |

1,725 |

57 |

Carbon Budget Order 2016 (SI 2016/765) |

|

6th |

2033-2038 |

In |

Preparation |

CCC to advise in December 2020 |

What I would like you to bear in mind (we will return to it later) is what the Committee on Climate Change (“CCC”) – a statutory consultee and provider of advice to the Government – says about the December 2020 advise to come, on its website, namely that:

“Advice on the Sixth Carbon Budget….

It will set the path to the UK’s new net-zero emissions target in 2050, as the first carbon budget to be set into law following that commitment”

As originally enacted, the target under s1 of the Act was that by 2050 reduction of CO2 emissions would have to be 80%. By affirmative resolution of the House of Commons on 12.06.19 this was increased to 100%. For the moment what I want you to note is that it is clear that the CCC considered that to be a watershed moment which may have led to an amendment in their thinking about the use of carbon credits.

-

This ever-reducing carbon budget was not something which the nation, as a nation, was not permitted to cap and trade in the same way in which nations may swap and trade their emissions with other nations under Kyoto: it constituted an ever lowering cap which simply had to be complied with under compulsion of law. Having said that, the UK’s emissions totals are the aggregate of emissions by individual emitters. Those emitters, as individual entities may seek, or be required to enter into, a cap and trade process which, in turn, requires the provision of emission allowances which can either be traded with peers for value or surrendered back to any regulating authority once the emissions which those allowance represent have occurred (the Secretary of State is empowered to set up such a system under ss 44 and 45 of the Act in respect of particular industries). Further detail as to what those schemes may consist of is set out in Schedules 2 and 3 of the Act.

-

Perhaps a little confusingly, the Act both refers to the emissions units which permit and record individual entity’s emissions (i.e. for the purpose of ‘cap and trade’) and the units representing carbon offsetting by the same phrase: ‘Carbon Units’. Although linguistically apt to confuse, the use of the same word is in fact entirely logical since it makes sense that the same thing which is being emitted is the same thing which is being offset against those emissions. Carbon units are defined within the Carbon Accounting Regulations 2009. I will return to the precise definitions later in this blog because they are important to issues of proof, but for the moment they can simply be thought of as being the equivalent damage to the planet to the emission of 1 tonne of CO2.

-

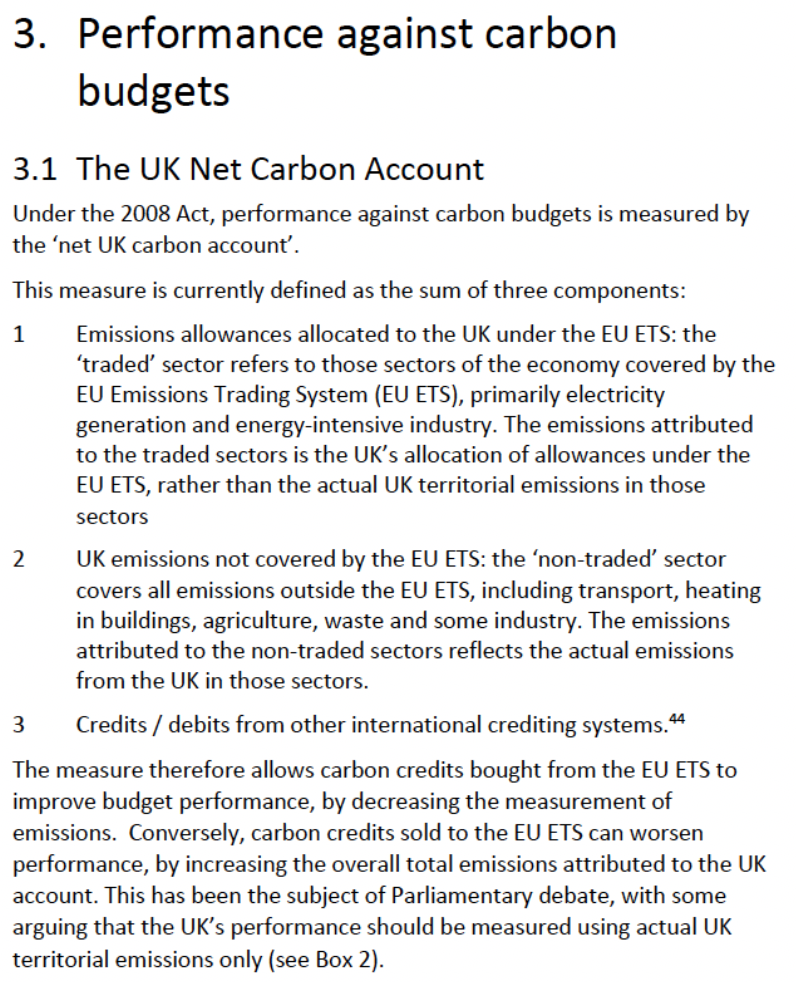

National accounting for emissions is to be done via the ‘UK carbon account’. This is defined by s27(1) but has been authoritatively described as follows:

Once a carbon unit has been used to offset the UK carbon account it may not be used again for any other purpose (i.e. a carbon credit can only ever be credited once) (s27(4)). International aviation and international shipping do not count towards the UK carbon account.

-

Perhaps in reality the most remarkable aspect of the carbon account is that the UK’s heavy industries covered by the EU-ETS have deemed emissions levels (that is the amount of emission allowances allocated to them by the EU) and not the actual level of emission. However, for the purpose of this blog, the issue we need to concentrate is the ability to rely, at least in part, in carbon credits created outside the UK as offsets against actual emissions in the non EU-ETS emissions sectors (for reasons outside the scope of this blog, EU-ETS does not permit the use of most offsets). The detail of carbon accounting is to be found in the Carbon Accounting Regulations 2009 (SI 2009/1257 and subsequent Orders in 2016 and 2020 – but the detail is not necessary for this blog.

-

In summary of this and past blogs on this, the nature of the relationships are as follow:

-

Kyoto/Copenhagen COP of the UNFCCC permitted/required Annex I countries to engage in ‘cap and trade’ limits.

-

The EU-ETS is a single reporting entity back to the UN for the entirety of the EU insofar as specified (usually heavy) industry is concerned. Where an industry is not covered by the EU-ETS directly, it falls within a wider pool of EU activity known as the ‘Effort Share Decision’. The UK has been a member of the EU-ETS hitherto and has implemented the EU-ETS domestically via the Greenhouse Gas Emissions Trading Scheme Regulations 2012.

-

The Climate Change Act 2008 represents the will of parliament to go beyond a cap and trade system represented by the EU-ETS and to set absolute limits for exposure for the nation (which reduce over time) as represented by the UK Carbon Account. The accounting system requires calibration to ensure that it is consistent with the ‘existing international systems which the UK is party to, in particular the EU ETS’. How that calibration operates in practice has been set out in paragraph 8 above.

-

In order to bring down the overall level of the UK Carbon Account in line with the UK’s domestic carbon budgets, polluting industries can be encouraged to reduce their emissions by the creation of domestic trading schemes for their industries (or collection of industries) (Section 44 and 45 of the Act). An example of this is the CRC Energy Efficiency Scheme Order 2013

-

At this stage we reach the nub of the blog. Section 11 of the 2008 Act places a duty on the Secretary of State to set a limit on the number of carbon units which may be credited to the UK carbon amount and upon the statutory Committee on Climate Change (set up pursuant to s32) to advise the Secretary of State in setting the limit of the setoffs permissible (s34(1)(b)(ii)). Section 27(2) requires that when calculating the UK carbon account and, in particular, when deciding to what degree carbon credits may be used to offset against the account, “The net amount of carbon units credited to the net UK carbon account for a budgetary period must not exceed the limit set under section 11’. In short, a limit is placed on the number of offsets which can be used in order to calculate the UK carbon account or, put another, a limit is put on the degree to which our country can pay others to reduce their carbon footprint and credit their efforts to our national target compliance.

-

The structures set up under the Climate Change Act do not naturally lend themselves to the idea that carbon offsets can form a substantial part of the solution of reducing carbon emissions. As we have seen above, if the basis of control is a ratcheting down of absolute emissions then it seems counter-intuitive to permit ‘backsliding’ by paying for someone else to reduce their carbon emissions (or increase their carbon sinks) at your expense and on your behalf. It is for this reason that s15 of the Act requires the Secretary of State to have regard to how targets can be met by domestic action to positively reduce emissions and increase carbon sinks and, as we have seen, s11 requires the setting of a limit to which carbon credits may be used to nett down actual emissions. However, as we have also seen, in fact trading is clearly permitted in other aspects of the operation of the UK Carbon Account (i.e. the trading of emissions which takes place in respect of EU-ETS and the specially constructed domestic CRC Energy Efficiency Market).

-

The initial position of the CCC was that outside the EU-ETS, there should be no traded carbon credits. The Government followed that advice for the first budget. The Climate Change Act 2008 (2020 Target, Credit Limit and Definitions) Order 2009 required that no carbon units could be credited to the UK carbon account unless they had arisen under the EU-ETS (Regulations 3(1) and 3(2)). However, this was reviewed in an impact assessment undertaken on 11.05.11. This review tested 3 scenarios: setting a very high limit for the use of carbon offsets, a nil limit and third a low limit of 55 million. The reasoning adopted was interesting. The pervading background was the strong belief in 2011, that the budget for 2013-2017 would be met and that hence there was not much justification for having substantial reliance on carbon credits which it was thought, might persuade the market that the UK was not serious about carbon offset. Without any allowance at all, then if the prediction about meeting the budget target suddenly looked inaccurate, the country might have to take very expensive steps suddenly in order to reduce absolute emission levels. Far cheaper would be the reliance then, on a small allowance of purchased carbon credits. On that basis the Climate Change Act 2008 (Credit Limit) Order 2011 set its face against the CCC and set the limit of reliance on carbon credits limited to 55 million carbon units over the accounting period. This was reflected in the Climate Change Act 2008 (Credit Limit) Order 2011. This is now the second straw in the wind to go with the reference I made earlier to the CCC considering that the setting of a challenging zero target for emissions in 2050 was an important watershed in their thinking on credits. The second straw is that where there was no belief that an emissions target would not be met, there was a corresponding lack of belief in the need for carbon offsets. Where those limits become more challenging, it becomes easier to see the need for offsets.

-

The UK continued a limit of 55 million carbon units for the third accounting period (2018-2022) and again this excluded the operation of the EU-ETS

-

Meanwhile the CCC maintained it disapproval of the use of carbon credits outwith the EU-ETS part of the UK carbon account. For example, in 2015 when setting their 5th carbon budget they stated that barring unforeseen contingencies “The budget should be met without the use of international carbon units (i.e. credits outside the EU Emissions Trading System”

-

However, I contend that beneath the waves, two tectonic plates were shifting, the combined effect of which was to change the view of the CCC in respect of carbon credits:

-

First, it was becoming clear that whilst the first three budgets had been/will be met (the third one is yet to expire) the fourth and fifth will not be met;

-

Second, the decision taken in June 2019 to reduce the overall target from 80% to 100% meant that some industries which were clearly incapable of becoming carbon free would have to achieve just that if the target was going to be met. In reality, 100% can only be achieved by reducing the rump of emission to the greatest degree practicable and then using offset for the rest.

Let me make good those assertions with evidence

-

The failure to meet the fourth and fifth budgets:

The 2018 Updated Energy and Emissions Projection 2018 issued by the BEIS has as its central case that the emissions total for the 4th budget will be 2,089 MtCO2e as against the limit of 1,950. The overshoot for the 5th budget is thought to be higher yet.

-

The change in tone of the CCC

-

In April 2016 and in the light of the Paris Agreement, the UK Government asked the CCC to advise on whether the overall target for 2050 should be reduced. In October 2016 the committee answered in the negative. However, in May 2019 the Committee published “Report on Net Zero: the UK’s contribution to stopping global warming” in which it did recommend a move to net zero and, with that move, came the change of tone. So what in 2015 had been an injunction from the committee “The budget should be met without the use of international carbon units” had softened by May 2019 to “The aim should be to meet the target through UK domestic effort, without relying on international carbon units” (p15) (emphasis added). A much stronger feel for ‘realpolitik’ can be seen elsewhere in the same document “If the speculative options to reduce UK emissions do not develop sufficiently, or if there is a shortfall in delivery of the other elements of the scenarios, then international carbon units (i.e. ‘credits’ or ‘offsets’) could provide contingency.

-

By the time of the June 2020 “Reducing UK Emissions Progress Report to Parliament Committee’ there is no statement at all to be found that carbon credits should not be used in respect of UK emissions targets. Indeed, there is an express emphasis that in future there will be an increasing need to rely upon them

“Over time, residual emissions will need to be offset by using verifiable, scalable engineered GHG removals (GGRs). DfT will need to work with BEIS in proposing a preferred mechanism for supporting GGRs in the UK including….interaction with international credits (p181)” and at p12 the explicit reference to the aviation industry requiring to rely on offsetting owing to the persistence of carbon use over time. Finally, this diagram taken from pp54/5 of the report.

There is reference to private companies not relying on them unless they have to, but again the tone is aspirational

-

Thus when Greg Clark MP, the minister steering the statutory instrument reducing the target to 0% on 12.06.19, in answer to Caroline Lucas MP that there would be no use made of credits, he was referring to advice from the CCC which appears to have changed – mainly in the light of that very vote by Parliament. The exchange is worth setting out.

-

Why do I set this out? Because in the final part of this blog, I want to consider to what degree there is any rationale for not using carbon offsets. The answer, I suggest, is firmly no.

-

First, the reason given by Ms Lucas MP is, with respect, clearly wrong. As I dealt with in the first blogs, a carbon credit can only be created pursuant to regulation and then can only be credited to the UK Carbon Account, if ‘additionality’ can be proven. I.e. it has to be shown that the act relied upon in either decreasing emissions or increasing carbon sinks, ONLY OCCURRED because someone was prepared to pay for it for the purpose of creating a carbon credit. Thus, a carbon credit cannot be taking ‘low hanging fruit’ which a third-party country would otherwise be using for a reduction in its own emissions.

-

There is ‘baked into’ the definition of what constitutes a ‘carbon unit’ i.e. for the purpose of being credited to the UK carbon account verification i.e. there is little chance for the carbon credit not being cleanly created provided it falls within the definition of what the UK calls a ‘carbon unit’.

-

What, then, is meant by ‘carbon units’? This is a crucial feature of the UK system.

(a) The Explanatory Notes to the (Credit Limit) Order 2016 make clear that the definition of ‘carbon units’ is to be found within the Carbon Accounting Regulations 2009 SI 2009/1257

(b) Regulation 3(1) of the 2009 Regulations defines ‘carbon units’ as including ‘certified emission reductions’ (“CER”) and these are further defined as “a unit issued under Article 12 of the Kyoto Protocol and the decisions adopted under the UNFCCC or the Kyoto Protocol”

(c) At first blush therefore, a ‘CER’ is limited to the unit which has been certified under the cumbersome and bureaucratic CDM system (i.e. one of the flexible systems under Kyoto). Whilst that would include afforestation and reforestation (Decision 17/CP.7) it is also the case that the phrase ‘…and the decisions adopted under the UNFCCC or the Kyoto Protocol’ is important here.

(i) The UNFCCC replaced Kyoto with a difference approach, namely that undertaken first at Copenhagen/Cancun (2009/2010) and then at Paris (2015). This new approach was dealt with in detail within my first set of blogs for Mere and so for our present purpose all which need be said is that it involved a move away from simply placing demands on Annex I nations and instead placing them on all countries (according to their economic ability) and a wide range of private actors within those countries.

(ii) The Paris Agreement is the present culmination of the process. Article 6.2 of the Paris Agreement allows countries to use “internationally transferred mitigation outcomes” (“ITMOs”) to achieve their mitigation targets provided that ITMOs shall “promote sustainable development and ensure environmental integrity and transparency, including in governance, and shall apply robust accounting to ensure, inter alia, the avoidance of double counting.”. This is the transferrable carbon credit. That forms one side of the equation.

(iii) The second side of the UNFCCC mandated equation is that of the adopt of REDD+ at Copenhagen/Cancun. Again, this was dealt with in more detail in my second series of interlinked blogs, and again, for our present purpose we can simply note that the intention was to provide capital flows to non Annex I countries, such as Ghana, in order for them set up internal systems for the avoidance of deforestation and the promotion of afforestation and reforestation. Those capital flows were to come in part from private parties and some of the economic lure for those flows would be the ability to use a wider series of validating bodies (i.e. beyond the CDM) to permit the carbon sequestered thereby to be sold back to sponsoring countries as a carbon credit.

(iv) When the two sides of the equation are synthesised, the following is arrived at:

-

-

REDD+ requires countries to ensure that deforestation (i.e. via illegal logging and sale) is prevented and that only identifiable timber from either afforested or reforested land is sold onto the international market

-

REDD+ requires those private actors carrying out afforestation/reforestation produce and sell ‘clean’ timber i.e. traceable timber grown in accordance with various principles of good governance

-

‘Clean timber’ sequesters carbon ‘cleanly’

-

Paris permits reliance upon third party verification of the ‘clean’ sequestration of carbon via reputable third parties (such as Verra who have both project based and – via its ‘Jurisdictional and Nested REDD+ schemes – country-based verification)

-

Since such verification is consistent with the decisions of the UNFCCC

-

Thus, carbon sequestered by the growth of clean timber and verified in by reputable third-party verification is capable of amounting to a CER which the UK government may add to the UK carbon account

-

-

In fact, I cannot see that the UK has ever credited a single tonne of carbon by purchase from a third party excluding the EU ETS pursuant to the register set up under Regulations 4 and 5. The documents setting this out are referenced below.

-

But it would now seem that there is no reason not to for the purpose of the Third accounting period, and very good reason to do so in the Fourth (commencing in 2022). For individuals and corporates, it is also a very good way of obtaining a stake in reducing the carbon footprint of us all.

-

In a later blog, I will deal with the effect of the UK’s withdrawal from the EU on all of the above. A copy of this blog will also appear at www.mereplantations.com

Michael Rawlinson QC

02.07.20